Nevertheless, if you wish to add additional riders to the brand-new policy, such as a long-term care rider, the company might need limited or complete underwriting. Amongst insurance policies, term life insurance coverage assurances payment of a specified survivor benefit if the insurance policy holder dies within the specified term period. Term periods may last anywhere from a year to 30 years. Importantly, term life insurance policies do not have financial or savings value unless the holder passes away within the term. However, term life insurance coverage might be less costly than other life insurance choices, such as whole life insurance coverage. Term life insurance coverage takes place over a fixed amount of time, usually between 10 and thirty years.

By contrast, whole life insurance covers the whole life of the holder. Unlike a term life policy, entire life insurance consists of a savings element, where the cash value of the contract accumulates for the holder. Here, the holder can withdraw or obtain versus the cost savings portion of their policy, where it can function as a source of equity. The holder will not have their money returned as soon as a term life insurance coverage policy ends if they outlive the policy. On the other hand, entire life insurance premiums might cost ten times more by contrast. This is since the risk to the insurer is much lower with term life policies.

" Life insurance coverage is method too complex! I'll fret about it when I'm older." We've all had comparable thoughts. Let's face it, everyone zones out of those life insurance infomercials due to the fact that they're ridiculously dull. However stick to us and we'll reveal you why term life insurance is the very best life insurance coverage alternative. Term life insurance coverage just suggests it lasts for a set number of years, or term. If you die before the term is over, the insurer will pay the death benefit (another way to say payment). If you die after the term is over, the insurer does not pay.

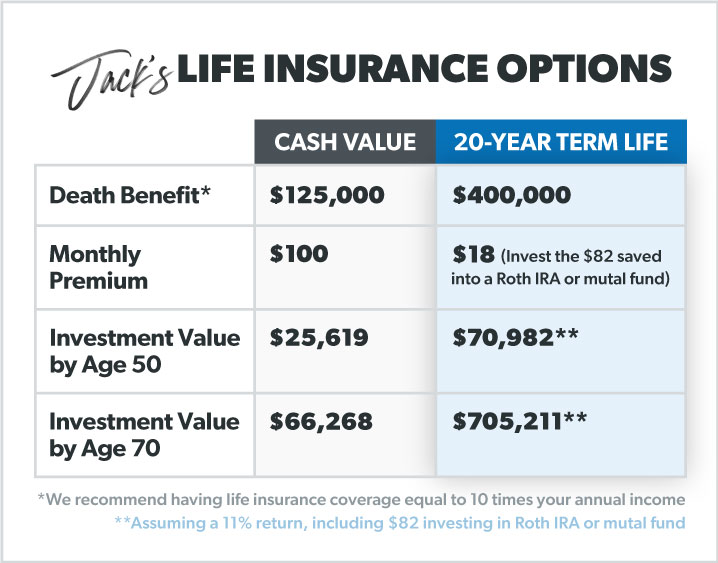

You require life insurance if you have a household or liked ones who depend on your incomebecause nobody lives forever. Life insurance coverage helps you offer them even after you're gone. It's not a great thing to think about, we concur. But making the effort to figure all of it out now is a million times smarter than leaving your enjoyed ones stranded if you suddenly died. Term life insurance works much like your car or house insurance coverage with a month-to-month payment, aka a premium. Let's look at a term life policy example for Steve, a healthy, non-smoking 30-year-old who makes $40,000 a year.

If he dies prior to his 20-year term is over, the $400,000 will go to his beneficiaries (his better half and 2 kids). Even though a beneficiary is most likely to be a liked one, it could also be legal guardians, your estate, a charity, or a legal trust (What is comprehensive car insurance). is understood as a permanent life insurance since http://paxtonpdjc873.trexgame.net/what-does-home-insurance-cover-for-beginners it remains in place for the entire of your life (and we hope that's into your 80s and beyond!). However that's a lot of premiums to payand high ones at that! We're talking 5-10 times more than a term life premium. Why are entire life premiums so high? Due to the fact that whole life insurance tries to act like a mutual fund (along with others in the money value insurance coverage household).

The Ultimate Guide To What Health Insurance Should I Get

So you are paying too much in the early years and constructing the money value to balance out the increasing expense of insurance in your later years. In truth though, when it comes to the "making money" part. Let's return to our buddy Steve. He likes to dabble in the stock exchange, but his insurance agent states if he goes with entire life insurance, his how to cancel timeshare premium will cover his life insurance policy and include investing. What the representative may not inform Steve is this: The quantity Steve makes if he goes with entire life is horrible compared to if he chose term life and put some cash on a monthly basis into another type of investment swimming pool (like a good shared fund).

Sadly, "riders" have absolutely nothing to do with horses or bikes in the interesting world of insurance coverage. Riders are additionals that "ride" on your regular term policy to function as a response to "what if" concerns like: What if we need to cover unanticipated funeral costs for a family member? What if I become disabled and can't pay my premium? One rider that may be worth having is one that covers funeral costs for your kid. However when it comes to riders like AD&D (accidental death and dismemberment) or important illness, getting some great will cover those things. And the truth is, other worries can also be covered by constructing an emergency fund of savings through.

You don't require to throw cash away to spend for a rider you don't require. And believe us, you'll fork out a lot since they'll acquire your premium to double what it should be. If you are nearing completion of the term of your policy, you could constantly renew the policy for another term. If you have a "level term" kind of plan (more on the types quickly) then your premium rate will increase when you renew (as you'll be older and more pricey to insure). There's also an opportunity your premiums could go down if you choose a lower survivor benefit.

It's easier than you think! If you put 15% of your home earnings towards investing, you won't require the survivor benefit by the time your term life plan ends since you'll have made a quite cent in financial investments. Okay, so here's where the majority of people want to check out because, well. insurance coverage. However take a deep breath and think and. To get the best of both, you'll desire to know the breakdown of all these different kinds of term life insurance coverage: Level premium term life insurance coverage makes certain the expenses remain level based upon the length of term you want (we suggest a term of 15-20 years).

That's a good feeling, isn't diamond resorts timeshare reviews it? This is the main reason Dave suggests level premium term life policies. You know exactly how much it's going to cost every time your premium is due and can work it into your budget plan - How does insurance work. Could insurance coverage actually be this easy? Yes! This one is a bit like level premium, except that the policy "renews" and the premium quantity increases every year until the term ends to cover the increasing expense of the insurance coverage. Precisely how much it increases by is determined the insurance provider when they measure your "threat" every year at renewal time (yikes!) This is a bit risky, and while it can seem inexpensive in the beginning - for about the first 5 years of your strategy - after that the premiums will come out greater than if you 'd chose a level premium term life policy.